A reply to “Global Cage-Free Markets: Opportunities and Challenges for The Hospitality Industry,” commissioned by the World Sustainable Hospitality Alliance and published March 2026.

Published by Accountability Lens Asia and co-signatories.

Executive summary

The WSHA’s March 2026 report argues its hotel members should receive extended timelines because Asian cage-free supply is limited and the cost of transition is prohibitive. We reject both premises.

Hotels have had nearly a decade — the urgency they now face is self-inflicted. The commitments were signed in 2016, 2017 and 2018. A cage-free farm transition takes six to eighteen months, so purchasing agreements signed as late as 2024 could have put physical supply on the plate by 2025. What companies have missed is not lead time. It is action.

Cage-free supply is growing in every major Asian market the report covers. Indonesia now has a national animal-welfare regulation and a dedicated cage-free producer association. Southern India operates one of the most functional cage-free ecosystems in Asia. Sundaily, China’s second-largest egg producer, is building the country’s largest single-site cage-free farm. Vietnam’s Nguyen Gia Livestock Cooperative completed one of the country’s largest cage-free transitions and received Certified Humane® certification in April 2026. Supply has been following demand. The demand has been signed for nearly a decade.

The cost of finishing the transition is a rounding error against the profits of every WSHA member. Hilton, Hyatt, IHG, Accor, Radisson, Four Seasons and Marriott each operate in the same Asian markets, buy from the same producers, and report annual net profits in the multi-billions. We work through the math for Marriott as a transparent example: at 345,922 Asian rooms and $2.601 billion in 2025 net profit, finishing the transition costs roughly $5.9 million a year — 0.23% of net profit — under conservative pricing, and stays under 1% even at the WSHA’s own most aggressive cited premium. The economics scale across the membership.

Franchise structure is a managerial choice, not a structural barrier. Franchise contracts already dictate pillow brand, coffee supplier and uniform vendor. McDonald’s USA — 95% franchised — hit 100% cage-free in 2023, two years ahead of its deadline. Hotel groups that want to enforce cage-free standards across their franchised properties can do so. They have chosen not to.

Cage-free credits are an established mechanism that hospitality peers are already using to deliver. Every major animal welfare organisation working at scale endorses well-designed credits with binding advance orders and jurisdictional integrity rules. Lagardère Travel Retail hit 100% cage-free globally in February 2026 using a physical-plus-credit blend. Best Western and Ascott have publicly accepted credits as part of their fulfilment path. The mechanism works when companies actually use it.

What remains is a choice, not a constraint. The WSHA report was commissioned by the hotel trade body whose members are the same companies that missed their 2025 deadlines. Its lead author discloses funding from the US United Egg Producers. No cage-free egg producers in Asia were interviewed for the report. Readers should weigh these things before citing it as evidence of industry-level obstruction.

Why this response exists

In March 2026, the World Sustainable Hospitality Alliance (WSHA) published a 49-page report on cage-free egg sourcing in hospitality. Its headline conclusions: hotels “are not responsible for creating cage-free supply and lack the capacity to do so on their own”; most companies will miss their 2025 cage-free commitments; and existing transition mechanisms — including credit-based systems — are of limited use.

The WSHA’s membership includes most of the global hotel groups whose public cage-free commitments have now lapsed: Marriott, Hilton, Hyatt, IHG, Accor, Four Seasons, Radisson, and others. Their collective procurement decisions affect the welfare of hundreds of millions of laying hens across the region every year. We work in Asia with the producers, buyers, and partners who actually move cage-free supply forward.

We strongly disagree with the conclusions of this report. What follows is our response, point by point.

1. Companies have had nearly a decade. Time is not the constraint.

The 2025 commitments cited in the report were not new. Marriott pledged cage-free in 2016. Hilton followed in 2017. IHG, Hyatt, and Accor had all made comparable commitments by 2018. That is seven to ten years of notice, set by the companies themselves after their own internal feasibility reviews, and in public consultation with animal welfare organisations.

A further extension is a request for a fourth or fifth bite at the same apple. It is a request to dilute a commitment that the same parties set, reaffirmed, and now find inconvenient. In the same window, these companies signed multi-year Power Purchase Agreements that financed renewable energy capacity which did not yet exist when the contracts were signed. They were willing to finance the construction of new wind and solar plants on the strength of their own commitment. Cage-free supply requires nothing of comparable difficulty — only a binding order at a known price.

Cage-free conversion is not a decade-long undertaking. Operational cage-free supply can be brought to market within eighteen months of a binding order — this is well understood at the producer level. Even a hotel group that waited until 2024 to place binding orders could have had physical supply on the plate by the 2025 deadline. Producers in our network describe a recurring buyer pattern — small initial orders, scaled up before audits, scaled back afterwards. The commitments were not missed because the lead time was insufficient. They were missed because companies did not place the orders.

Bill Bernbach, the advertising executive, once said “a principle is not a principle until it costs you money”. A commitment is no different: it means nothing until it is inconvenient. These commitments have become inconvenient — which is the moment that tests whether they ever meant anything at all. 1

A principle is not a principle until it costs you money

Bill Bernbach

2. Asia’s cage-free supply is growing, country by country.

The report treats Asian supply as a static constraint. The evidence on the ground is different: supply is not only present, it is expanding, and the rate of expansion tracks the commitments buyers have actually signed.

Indonesia. In 2019, cage-free production was a handful of small producers. By early 2026, roughly 20 dedicated cage-free farms operate across Java and Bali, the Ministry of Agriculture has issued an animal-welfare regulation (Permentan 32/2025), and a dedicated Indonesian Cage-Free Association (ICFA) now represents producers and coordinates with buyers.

India. Southern India is one of the most functional cage-free ecosystems in the region, with commercial-scale producers in Tamil Nadu, Karnataka, and Andhra Pradesh. Producers are organised and represented by the Cage-Free Free-Range Poultry Producers’ Association (CFFRPPA). The WSHA report itself (p. 29) concedes that hybrid sourcing models “have been especially effective in Southern India,” before spending later pages casting doubt on hybrid models. Compass Group is directly supporting transition at three Indian farms, and is co-funding a cage-free producer training facility in South India.

China. China produces roughly 40% of the world’s eggs. The report’s 10% cage-free share figure is the right baseline, but it omits what has happened on top of it: Sundaily, China’s second-largest egg producer, is now building the country’s largest single-site cage-free farm. Ovodan Egg Group has plans to produce 300 million cage-free eggs per year. After a succesful pilot in East China, Sun Art Retail (RT mart) is now expanding cage-free egg distribution to southern stores, totally 234 stores nationally. They saw 200% year on year growth in cage-free egg sales, dispelling any myth that demand is lacking. A national cage-free standard is in force, and multinational buyers at commercial scale — including IKEA — are sourcing cage-free eggs from Chinese suppliers today.

Vietnam. The Nguyen Gia Livestock Cooperative in Northern Vietnam — an existing caged-egg farm that has now transitioned its full 50,000-hen flock to cage-free housing in partnership with Global Food Partners — received Certified Humane® certification in April 2026, in what the certifier and GFP describe as one of the largest cage-free transitions in Vietnam and across Asia. It is a commercial-scale proof point in the country that transition financing, third-party audit, and cage-free buyer demand can come together in a Southeast Asian producer market.

The pattern across these countries is consistent: supply follows committed demand. Where buyers place binding orders, producers expand. Companies that have treated their commitments seriously are delivering — Lagardère Travel Retail reached 100% cage-free globally in February 2026 using a 62% physical, 38% credit blend in Asia; Capella Hotel Group is 100% cage-free across their 14 hotels and properties, majority of which are in Asia; and Pizza Express has reached 100% across its operating regions, including several in Asia.

3. Hospitality has built harder supply chains than this.

The report’s central premise is that hotels lack the capacity to build cage-free supply. The same industry, over the past decade, has built on-site solar and negotiated renewable-energy contracts in markets with underdeveloped grids; developed MSC- and ASC-certified seafood supply in countries where third-party-audited fisheries did not previously exist at commercial scale; sourced deforestation-free palm oil and paper across Southeast Asia under intense scrutiny; and designed water-stewardship infrastructure in water-stressed regions.

None of these supply chains existed at scale when hotels first committed to them. They were built because companies treated their commitments as binding and worked with producers, finance partners, and certifiers to create capacity. The argument that eggs are uniquely impossible does not survive a side-by-side comparison with carbon, water, or seafood. What survives is a question of priority.

4. Consumers are not responsible for delivering corporate commitments. Corporations are.

The report leans on consumer willingness-to-pay: diners will not absorb a premium, passing cost through risks competitiveness. This is not a supply-side argument. It is a pricing argument, and it is addressed to the wrong party.

Hospitality companies operate corporate social responsibility, ESG, and sustainability functions precisely because markets do not self-correct on animal welfare. A public cage-free commitment is, by its very structure, an admission that the company bears responsibility to shift the market — not to follow whatever signal diners happen to send at the buffet. Shareholders and boards, not diners, approved these commitments. Asking diners to now ratify them separately is, in effect, an argument that ESG commitments mean nothing unless customers vote for them at the point of sale.

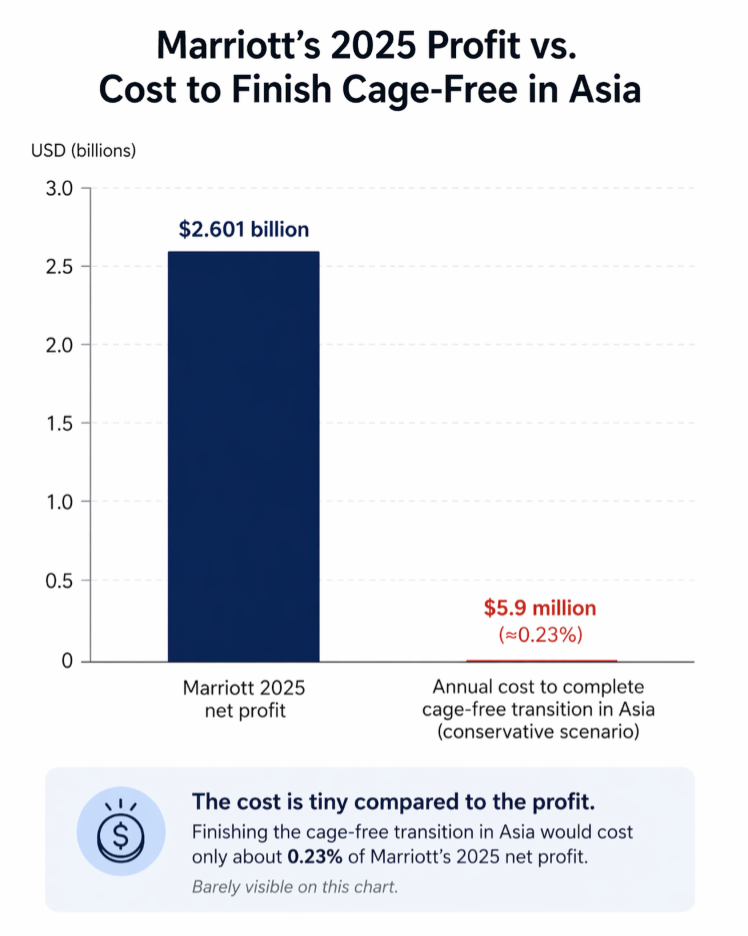

5. The cost of cage-free is a tiny fraction of their corporate profits.

The cost of finishing the cage-free transition is minuscule compared to hotel profits. Footing the bill would cost them almost nothing.

Take Marriott International, the largest hotel group represented in the WSHA, as an example. In 2025, Marriott reported net profit of $2.601 billion on ($26.186 billion in revenue). We conservatively estimate that a full cage-free transition in Asia would cost Marriott approximately $5.9 million per year — roughly 0.23% of 2025 net profit. That estimate uses a 100% cage-free premium, which sits well above the 30–60% wholesale cage-free premiums typical in Asia producer markets today. Even when we instead use the highest premium figure cited anywhere in the WSHA report — 300% for “developing markets” — the cost remains under 1% of 2025 net profit. See the full methodology in the appendix below.

Marriott 2025 profit vs cage-free transition cost

Full scenario range:

| Premium assumption | Source | Annual cost | % of 2025 net profit |

| 20% | US California Prop 12 retail pass-through (WSHA p.30 cites 17–33%; we use the low end) | $1.2M | 0.05% |

| 100% | Conservative headline anchor — well above 30–60% typical Asia wholesale premium | $5.9M | 0.23% |

| 300% | Upper bound of WSHA’s “developing markets can reach 80–300%” (p.34) | $17.6M | 0.68% |

| 300% × 100% of Asia volume (ignore already cage-free) | Absolute stress test | $26.5M | 1.02% |

Even the absolute stress case — the WSHA’s highest premium figure applied to every egg Marriott buys in Asia, ignoring the ~33% already cage-free — costs almost exactly 1% of annual net profit.

Marriott is used here as an example, but the economics are the same for every major hotel group. Hilton, Hyatt, IHG, Accor, Radisson, Four Seasons and the rest operate in the same Asian markets, buy from the same producers, face the same premium range, and report profits in a similar order of magnitude. For any of them, the incremental cost of finishing what they promised is a rounding error on the income statement.

If companies disagree with any of these numbers, they would be welcomed to disclose the actual increased cost per unit sold, which they never do even though they always cite costs and consumer willingness to pay as excuses. This is not a close call. These hospitality companies can easily absorb this cost.

6. Hotels already collected the reputational dividend. Without delivery, that is humane washing.

The cost debate pretends there is only one side of the ledger. There is another.

For nearly a decade, every major hotel group has listed its 2025 cage-free commitment in its ESG reports, sustainability disclosures, investor decks, and press releases. The commitment earned them positive coverage in trade and business press. It fed into Dow Jones Sustainability Index placement, MSCI ESG ratings, and Bloomberg ESG scores that investors and asset managers use to allocate capital. It gave their ESG teams a line item to present to boards and donors. It allowed them to sit on sustainability panels alongside peers who had actually delivered.

That reputational dividend was not hypothetical. It was collected — year after year — for a commitment that most of these companies never physically delivered on by their own 2025 deadline.

Making a commitment, enjoying the brand credit, and then quietly missing the delivery is textbook humane washing – a form of greenwashing. Animal welfare organizations are right to call it that, and right to keep calling it that. A company that accepted a decade of upside from a promise does not get to treat the downside of breaking it as unfair pressure.

7. Franchise structure is not a legitimate excuse.

The report notes, correctly, that global hotel groups operate a mix of managed and franchised properties, and implies this complicates delivery.

Franchise agreements in global hospitality already specify brand standards at extraordinary granularity: bed linen thread count, in-room coffee supplier, check-in software, amenity brand, minibar inventory, uniform vendor. A company that can mandate the pillow a guest sleeps on across thousands of franchised properties can mandate the eggs served at breakfast. It has chosen not to.

The clearest proof point is McDonald’s USA: approximately 95% franchised, roughly 13,000 restaurants. McDonald’s USA committed to 100% cage-free in 2015 and achieved the goal in 2023, two full years ahead of deadline, sourcing nearly 2 billion eggs annually. Cargill financed a significant part of the transition, extending producer transition capital and long-term contracts that let egg farmers secure construction financing.

When a heavily franchised burger chain delivers on cage-free two years early, a global hotel group with a centralised corporate sustainability function does not get to cite its franchise model as a structural barrier.

8. Credits are a recognised mechanism. Animal welfare groups endorse them. So do hospitality peers.

Cage-free credits are not a fringe workaround. Every major farm animal welfare organisation working at scale — The Humane League, Compassion in World Farming, Mercy For Animals, the Open Wing Alliance — recognises well-designed cage-free credits as a legitimate mechanism for accelerating the transition, provided they include binding advance orders and jurisdictional integrity rules.

Investors also support the use of credits. Investors expect adequate animal welfare, and annual progress reporting, specifically of % eggs that are cage-free as per SASB standards for restaurants and retailers as part of existing disclosure frameworks

Companies across sectors, including hospitality, have reached the same conclusion and acted on it. Lagardère Travel Retail, operating 4,900+ stores across 50+ countries, hit 100% cage-free globally in February 2026 using a 62% physical, 38% credit blend in Asia, and publicly reported the breakdown. Compass Group, the world’s largest foodservice provider, is delivering cage-free in India through a combination of physical sourcing and credits, having recently purchased 4 million eggs worth of credits. Kellanova and Pizza Express use the same framework. Best Western and Ascott have publicly accepted cage-free credits as part of their fulfilment strategy.

Credits are a bridge, not the destination — advance orders fund producer transition, and the volume is expected to convert to physical supply over the life of the contract. Companies using credits are not conflating them with physical eggs in their reporting — Compass Group’s 2025 Animal Welfare Progress Report and PizzaExpress’s sustainability disclosures both separate physical from credit-supported volume line by line.

The WSHA report’s skepticism about the integrity of credits does not square with the position of the organisations that have spent the most time studying them, nor with the decisions of the hospitality companies already using them to deliver. The mechanism exists. It is endorsed by both sides of the buyer–advocate table. Companies that want to deliver are delivering.

9. What the report leaves out.

Three omissions a reader should be aware of.

No producer voices. The report does not interview a single cage-free egg producer in Asia, or any farmer beneficiary of a transition programme, or any cooperative representative. A 49-page report on whether cage-free supply can expand in Asia, written without asking any Asian producer, is a report with a structural blind spot.

The lead author’s funding disclosure. Dr Vincenzina Caputo discloses, on page 5, that her research programme is supported by “commodity organisations such as the United Egg Producers and the United Soybean Board.” The United Egg Producers is the primary US trade association representing conventional-cage egg production. We take no position on whether this funding shaped any specific conclusion. We note the disclosure because disclosure exists for a reason.

The commissioning party. The WSHA is funded by its member hotel groups, the same groups whose 2025 commitments have lapsed. When a trade body commissions a report, pays for it with member dues, and the report concludes those members’ failure was largely outside their control, the conclusion was predictable from the brief. That does not make it worthless — but it does mean it should not be mistaken for a neutral assessment. It is a document shaped by what the commissioning parties want to hear.

The bottom line

Millions of laying hens across Asia remain in battery cages today because the largest hotel groups in the region have decided that keeping their money is worth more than keeping their word. The WSHA report is a well-funded effort to make that trade-off easier to defend in public. We are writing this so that it gets harder, not easier.

The facts, as we read them, are these:

- Companies have had nearly a decade.

- Supply is growing in every Asian market they operate in.

- The mechanisms to close remaining gaps (like cage-free incentives) exist, are endorsed across the animal welfare sector, and are being used successfully by corporate peers.

- The incremental cost for a company like Marriott is a fraction of a percent of annual net profit.

- Franchise structure is not a barrier.

Once supply, cost, mechanism, and structure are off the list of plausible explanations, one remains: these companies chose to keep the money. Given the scale of that money relative to the scale of harm to the hens, that is not a defensible reason.

We will continue to say so, publicly and by company name, until the deliveries arrive.

What to do if you are a hospitality company

We have no interest in punishing companies that are honestly working the problem. We are interested in distinguishing them from companies using this report as cover.

If your company is serious, four things belong on the table this quarter:

- Publish an updated, country-specific cage-free roadmap for Asia-Pacific, with physical and credit components broken out and a fixed new completion date. Given that lead times on farm conversion are 6 to 18 months and that supply exists today in every major Asian market, a serious roadmap should target full delivery within the next 12 months, not in three to five years.

- Place binding advance orders with cage-free producers in the countries where you operate. Supply cannot just appear. It is built by buyers who fund it into existence, the same way your company does in renewable energy.

- Disclose 2025 delivery honestly, country by country. If you missed, say by how much, in which markets, and what you will do in the next 12 months to close the gap. “Progressing” is no longer a credible report-out for a commitment made nearly a decade ago.

- Engage the country-level animal welfare organisations working on your supply chain. We have producer relationships, transition-finance partners, and audit infrastructure. A 30-minute call is a cheaper due diligence step than another commissioned report.

What to do if you are a supporter

If you are a customer, a loyalty-programme member, a shareholder, or simply someone who thinks companies should honour public commitments, join our digital accountability campaign team. We send out weekly actions you can take — email templates, social posts, specific company targets — to hold hospitality companies accountable for the promises they have made. Five minutes a week. Real pressure, applied at the points where it changes decisions.

Co-signatories

This post is open for endorsement by animal welfare organisations, country initiatives, and allied civil society groups working across Asia. Draft circulated to partner organisations for sign-on ahead of publication. To add your organisation, contact info@accountabilitylens.org .

- Accountability Lens Asia

- Bharat Initiative for Accountability

- Indonesia Network for Compassionate Animal Farming

- Vietnam Animal Welfare Watch

- Planet for All

- Malayang Manok Philippines

- Farmed Animal Compliance Thailand

- Malaysia Accountability Project

Methodology appendix — the Marriott cost estimate

A transparent back-of-envelope calculation. Every input is public; every assumption is stated; any reader who disagrees with a single input can substitute their own.

Rooms. Marriott operates 345,922 rooms across Asia (Greater China plus Asia Pacific excluding China), per its 2025 Form 10-K.

Egg volume. Rooms × benchmark rate of 1 egg per room per day × 365 days. The one-egg-per-room-per-day rate is a mid-range estimate of a full-service hotel’s total egg use (shell eggs served at breakfast plus eggs used in cooked dishes, baking, and banqueting), expressed per occupied-equivalent room per day. Plausible range: 0.5 to 2 eggs per room per day. The mid estimate yields approximately 126 million eggs per year in Asia (345,922 rooms × 1 × 365). The low end (63M) and high end (253M) do not change the conclusion — even at the high end, the total cost sits well below 1% of 2025 net profit.

Current cage-free share. Marriott’s 2025 Global Progress Report discloses 2024 cage-free spend of 52% in Asia Pacific excluding China and 49% in Greater China. Because cage-free eggs cost more per unit than caged, a spend share of ~50% translates into a lower volume share. Under the premium range used below, Marriott’s already-cage-free Asia volume works out to 33–43%. We conservatively apply the low end — a blended 33% already-cage-free volume share — so our “remaining” volume (and therefore our cost estimate) is as high as the inputs reasonably allow. Remaining volume to transition: approximately 84 million eggs per year.

Baseline caged egg prices, 2025–2026 wholesale, with per-country working shown so any step can be verified:

India — ~$0.049 / egg – Source: Today Egg Rate India — National Egg Coordination Committee (NECC) daily wholesale rate – Price: ₹4.20 / egg wholesale – USD/INR: ~85 – ₹4.20 ÷ 85 = $0.0494 / egg

Indonesia — ~$0.095 / egg – Source: Badan Pangan Nasional monthly national producer price dataset – Price: Rp 26,027 / kg (national producer price, January 2026) – Eggs per kg @ 60 g each: 1000 ÷ 60 = 16.67 eggs/kg – Rp 26,027 ÷ 16.67 = Rp 1,561 / egg – USD/IDR: ~16,400 – Rp 1,561 ÷ 16,400 = $0.0952 / egg

China — ~$0.070 / egg – Source: Beijing Xinfadi Wholesale Market daily price board (category: 肉禽蛋 → 筐鸡蛋 / crate eggs) — China’s largest agricultural wholesale market, referenced by the Ministry of Agriculture and Rural Affairs and state media – Price: 4.22 CNY / 斤 (jin), 24 April 2026 – 1 jin = 0.5 kg, so 4.22 CNY / 0.5 kg = 8.44 CNY / kg (unit is unambiguous on the Xinfadi board, shown on every row as 单位: 斤) – USD/CNY: ~7.2 – 8.44 CNY ÷ 7.2 = $1.172 / kg – $1.172 / kg × 0.060 kg/egg = $0.0703 / egg

Weighted blended baseline: approximately $0.07 per egg. Simple mean of the three is $0.0716; we round down to $0.07 for clean math. Marriott operates in additional Asian markets beyond these three; their wholesale prices fall within the same band.

Cage-free premium. Every premium figure in the table above is a figure cited inside the WSHA report itself, so the conclusion does not depend on our pricing data:

- 20% (floor). The WSHA report (p. 30) cites the California Proposition 12 retail pass-through study: “retail egg prices increased by 17–33%.” We use the low end (20%) as the floor.

- 100% (headline anchor). Not a figure quoted directly in the WSHA report. Used because it sits clearly above the typical 30–60% wholesale cage-free premium seen in Asia producer markets today (per producer-network data across India, Indonesia and Vietnam), and well below the report’s cited upper bound. A round, defensibly conservative number.

- 300% (upper bound). WSHA p. 34: “price premiums in developing markets can reach 80–300%.” We use 300% as the extreme upper bound so a skeptical reader cannot collapse the argument by citing the report’s most aggressive figure.

Marriott 2025 financials. Net profit $2.601 billion on $26.186 billion in revenue, from the Q4 / full-year 2025 earnings release. Implied daily profit: $7.13 million.

Sensitivity. Doubling the eggs-per-room rate, doubling the baseline price, or halving the already-cage-free share each roughly doubles the cost. The conclusion — that the incremental cost sits at or below 1% of annual net profit even in the most unfavourable scenario — holds under every individual stress test we have applied.

For media enquiries, corporate dialogue, or to add your organisation as a co-signatory, contact Accountability Lens Asia at info@accountabilitylens.org.

- When asked by reporters why he would not do business with tobacco companies and forgo the profits, Bernbach replied: “It was a matter of principle and it cost us money — cigarette advertising is the most profitable kind you can have. But I don’t feel a principle is a principle until it costs you money.” ↩︎